Kase HedgeModel

Statistical Decision Support for Energy Hedging

The Kase HedgeModel is a proven, rule-based hedging system built on sound mathematical, statistical, and engineering principles. It identifies statistically low-risk areas for hedge execution — helping producers and consumers reduce price risk while maximizing the probability of meeting their hedge plan goals.

Built for Energy Producers and Consumers

The Kase HedgeModel serves commercial energy market participants who need a systematic, statistically grounded approach to hedge execution — replacing guesswork and timing intuition with a disciplined, probability-based framework:

Oil and Gas Producers

Identify statistically favorable price levels to lock in revenue through fixed-price hedges, capturing attractive prices when they arise without missing opportunities.

Energy Consumers and Utilities

Systematic guidance for purchasing price protection on natural gas, crude oil, and refined products — minimizing cost exposure without over-hedging at unfavorable prices.

Pipeline and Midstream Companies

Probability-based hedge triggers for managing commodity price exposure embedded in transportation, storage, and processing operations.

Energy-Intensive Industrials

A structured hedging framework for manufacturers, chemical producers, and other large energy consumers managing fuel and feedstock price risk.

Airlines and Transportation Companies

Fuel cost risk management support through statistically derived hedge triggers for jet fuel, diesel, and related refined product markets.

Finance and Treasury Teams

A systematic, auditable hedge decision framework that supports internal governance requirements and board-level reporting on commodity risk management.

A Proven, Probability-Based Approach to Hedge Execution.

Successful long-term hedging requires logical, systematic decision-making. Any rational program must consider the market’s underlying structure and longer-term behavior to identify points that minimize risk and maximize the results of a hedge plan. Ad hoc or calendar-based approaches leave too much to timing and intuition, and tend to result in hedges placed at unfavorable prices.

The Kase HedgeModel is built on the observation that most commodities, including energy, exhibit mean-reverting characteristics over the long run and tend to conform to log-normal price distributions. This statistical structure allows the model to make specific, mathematically grounded judgments about current prices in relation to the central tendency of the market as a whole and identifies when prices are statistically favorable for hedging and when they are not.

The model functions on natural gas, crude oil, refined products, and custom data. It is accessed via Kase Access, a secure web portal on the Kase website, allowing users to view the HedgeModel charts from any computer without a live data feed.

How the HedgeModel Works

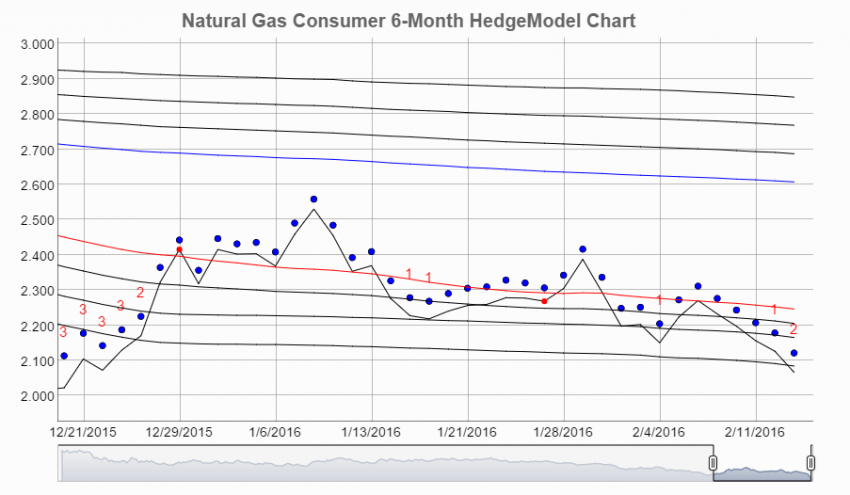

The HedgeModel evaluates forward curve strip data to generate statistically derived hedge triggers and displays them as Scales and Bands on charts accessed through the Kase Access web portal. Two types of strips are used: traditional strips to generate the statistically significant hedge levels, and modified strips (beginning with the second nearby contract) to trigger and place the hedges.

Kase HedgeModel — Scales and Bands plotted on a natural gas forward strip, showing statistically derived opportunistic and protective hedge trigger levels.

Opportunistic Scales — Capturing Favorable Prices

The Scales are placed at statistically significant levels away from the historic mean and define the most favorable area of hedging. They trigger when prices reach levels that are statistically attractive: high prices for producers, low prices for consumers. Hedgers scale into positions gradually as each Scale level is breached, placing a percentage of total volume based on their risk appetite at each trigger rather than committing all at once.

- Three Scale levels trigger sequential portions of the hedge — typically up to 50% of total volume as prices are moving in a favorable direction

- Each Scale calls for approximately 5% of volume per day up to a given limit based on the hedger’s risk appetite and strategy

- A warning Scale alerts the hedger as prices approach the trigger Scales

- Remaining volumes are hedged at an accelerated pace on a reversal in the opposite direction

- Separate Scale configurations for producers and consumers

Price Zones

The HedgeModel divides the price environment into three zones that determine the appropriate hedging posture at any given time:

- High price zone — prices at or above producer Scales or consumer Bands; favorable for producers, protective strategies for consumers

- Neutral zone — prices between upper and lower triggers; neither statistically favorable nor unfavorable for hedging

- Low price zone — prices at or below consumer Scales or producer Bands; favorable for consumers, protective strategies for producers

Protective Bands — Buying Price Protection

When prices are unfavorable — too high for consumers or too low for producers to be considered attractive — the Bands identify levels at which option-based protective strategies are warranted. Rather than fixing prices at unfavorable levels, hedgers use options to protect against a worsening situation while retaining the ability to benefit if prices improve.

- Consumers buy calls as the strip rises through consumer Bands

- Producers buy puts as prices fall through producer Bands

- Three Band levels trigger sequential option purchases at graduated rates

- A warning Band alerts the hedger that prices are approaching the trigger Bands

Included: Kase Commentary on Crude Oil or Natural Gas

Every HedgeModel subscription includes a complimentary subscription to the corresponding Kase Commentary — either the Commentary on Crude Oil or the Commentary on Natural Gas, depending on the market you are hedging.

The Kase Commentary delivers weekly probability-based technical analysis of the same market your HedgeModel covers — providing independent price direction intelligence, exact targets, and Monte Carlo simulations that give essential market context alongside your statistical hedge triggers.

- Weekly Commentary on Crude Oil or Natural Gas

- Daily market updates Monday through Thursday

- Probability-weighted price targets and dual-scenario analysis

- Monte Carlo simulations across five price scenarios

- Direct analyst access for questions about the analysis

Five Hedge Categories. One Framework That Fits Your Goals.

Since different organizations have fundamentally different hedge objectives, the Kase HedgeModel is configured around five distinct hedge strategy categories. Each is calibrated to a different risk appetite and business orientation. Customization services are also available for specific client needs:

Very Aggressive

Maximum protection orientation. Hedges are placed at the earliest possible trigger levels, prioritizing coverage over price optimization. Appropriate for organizations with critical cash flow or budget exposure to adverse prices.

Aggressive

Primarily cash flow driven. Defensively oriented to avoid adverse prices. Willing to accept higher hedge costs to ensure protection. Does not tolerate missing a hedge opportunity.

Moderate

A balanced approach between opportunistic price capture and protective coverage. Calibrated for organizations that require both budget certainty and some ability to benefit from favorable price moves.

Conservative

Primarily revenue or cost-capture driven. Hedges only when statistically attractive prices arise. Willing to miss hedges and accept adverse pricing periods in order to avoid unnecessary hedge costs.

Very Conservative

Opportunistic only. Hedges are placed exclusively at the most statistically favorable price levels, with minimal use of protective strategies. Appropriate for organizations with high tolerance for price risk and low hedge cost budgets.

Custom Configuration

For organizations with specific requirements not met by the standard five categories, Kase offers customization services to develop a model configuration aligned precisely with your hedge plan and governance framework.

Markets Covered and Kase Access

The Kase HedgeModel operates across all major energy commodity markets and is delivered via a secure, web-based portal that requires no software installation or live data feed:

Markets Covered

- NYMEX Natural Gas — multiple strip lengths from three to twelve months

- WTI Crude Oil and Brent Crude Oil

- NY Harbor ULSD and RBOB Gasoline

- Custom data — proprietary forward curves or alternative market structures

Hedge Instruments Supported

- Fixed-price swaps and futures (Scales — opportunistic hedging)

- Call and put options (Bands — protective strategies)

- Collars and structured option strategies

Kase Access — Web Portal Delivery

- No software installation required — view HedgeModel charts from any computer or device

- No live data feed required — Kase manages all data inputs and model updates

- Charts are updated daily and available on demand through the portal

HedgeModel Features

- Identifies high-probability hedge points automatically

- Differentiates between attractive and protective hedging situations

- Includes overlay of technical indicators for in-depth market analysis

- Identifies when to hedge, which maturity to use, how to scale in, and when to restructure

Subscription Options

HedgeModel Subscription

Established through a subscription agreement. Invoiced directly with payment by wire transfer or check. Contact us for details on discounts available for longer terms, multiple commodities, or combined subscriptions.

| License Type | Coverage | Monthly Rate |

|---|---|---|

| Standard License | Single user | $3,000/month |

| Site License | Unlimited users, one location | $4,400/month |

| Enterprise License | Unlimited users, all locations | $6,500/month |

Included With Every Subscription

Every HedgeModel subscription includes a complimentary subscription to the Kase Commentary on Crude Oil or Natural Gas — giving subscribers independent weekly technical analysis of the same market their HedgeModel covers.

Contact us to discuss which license tier fits your organization and to ask about discounts for longer terms or multiple commodity subscriptions.

Rigorous Statistical Foundations. Since 1992.

The Kase HedgeModel is built on the same statistical and engineering discipline that underlies all of Kase’s analytical work — not rule-of-thumb timing or calendar-based hedging programs. The model’s foundations include:

- Mean reversion theory — exploiting the long-run tendency of commodity prices to revert toward statistical norms after extended moves in either direction

- Log-normal price distribution modeling — establishing statistically defensible probability estimates for prices at varying levels above and below the long-run mean

- Multi-timeframe standard deviation calculations — short, medium, and long-term lookbacks for Scale and Band placement, returning the most conservative price objective across all timeframes

- Strip-based analysis — forward curve data evaluated on modified strips commencing with the second nearby contract to ensure hedge ranges reflect actual executable prices

- Rule-based, mechanical framework — all trigger levels are algorithmically derived, producing an auditable and repeatable hedging process with no discretionary override of statistical signals

The Kase HedgeModel is a statistical decision support tool designed to inform and support each client’s own hedge execution decisions. It is not to be construed as investment advice, trading recommendations, or consulting. All hedging decisions remain the responsibility of the individual organization and its advisors.

Request a No-Charge Trial

Experience the Kase HedgeModel for your market and see how a statistically grounded hedge trigger system compares to your current approach — at no charge and no obligation.